Inversions: Finance Runs on Math That Was Wrong From the Start

Signal 054. The market is not malfunctioning. The math was reversed before anyone ran it, built to multiply on a substrate it cannot see, the collapse you are watching is the model arriving on time.

You have probably been taught that the financial system will always be there and that the right institutions are there to catch it when it falls. The Federal Reserve has the tools, and the economists have the model, and the markets are mostly efficient, and when they are not, smart people step in. I bet you truly believe recessions are the disease, and growth is the cure, the stock market is a thermometer. When it rises, things are fine. When it falls, we should worry but not panic. Someone in a corner office or on the trading floor somewhere is handling it.

But I have news for you… This inversion series has really taught me something:

The data underneath the story is overwhelming. The Federal Reserve balance sheet has expanded from $900 billion to $9 trillion dollars between 2008 and 2022. Sovereign debt past $35 trillion. Interest on the federal debt now exceeds defense spending. Roughly one in five public companies in developed markets cannot cover its interest from earnings. The top 1% holds 32% of US wealth and 86% of stocks. Median real wages have been roughly flat since 1979, while productivity has roughly doubled. The whole architecture of capital is being held up by the same intervention that was supposed to be temporary in 2008 and somehow became permanent.

And this is only the current view.

A managed financial system whose stability is the policy and whose volatility is the embarrassment, run on math that has been demonstrably wrong for sixty years, producing crises on a regular cadence that the system calls exceptions. It is reading the symptom as the disease. It has been doing that since 1971 when the gold standard ended. The bodies are now telling us what that has cost.

What’s Happening Beneath the Surface

Now turn the reading.

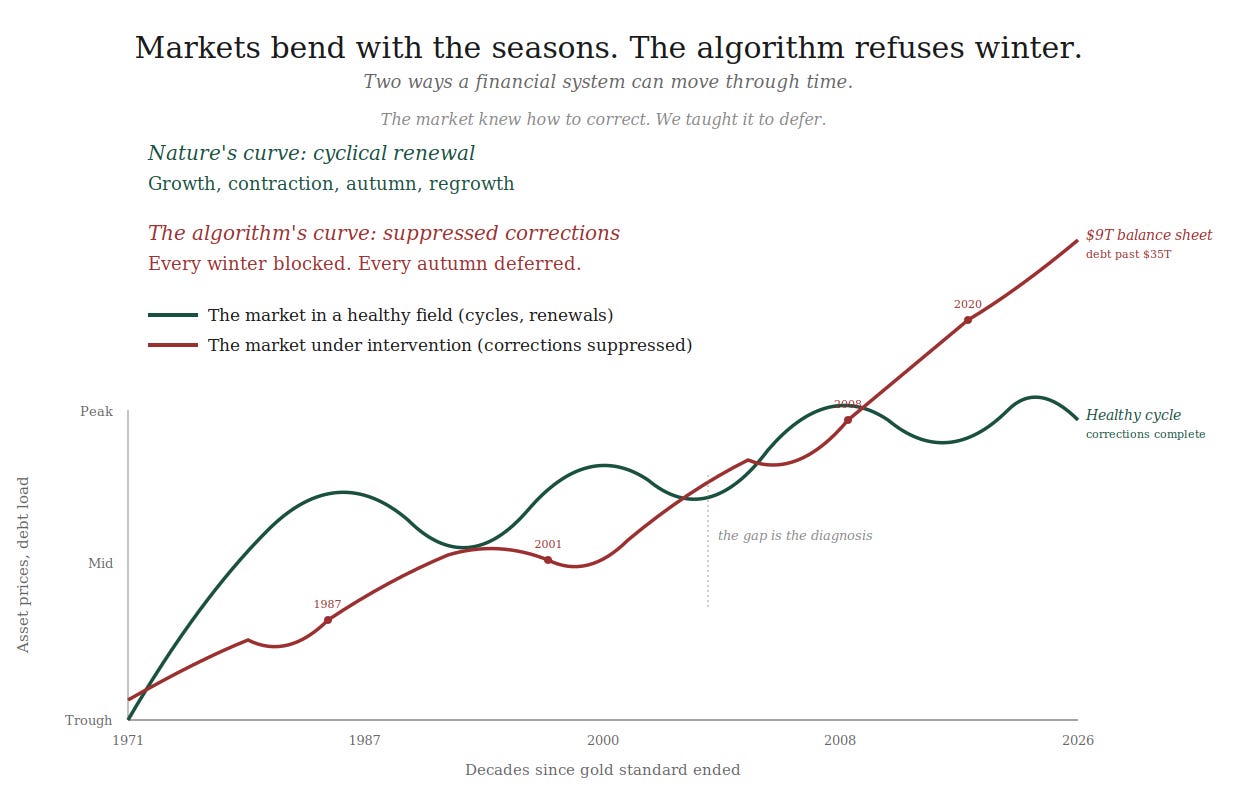

The market is doing exactly what every other living system does, and the math the industry uses to describe it has been wrong since the day it was written. Markets are not normal distributions. Markets are fractal. Benoit Mandelbrot demonstrated this in 1963 and called it the scandal of finance, and he was largely ignored for forty years because his math was harder than the equilibrium math the industry had already built. Real markets generate fat tails. They produce events the Gaussian distribution says happen once every thirteen thousand years, and they produce them every decade or so, because the underlying system is not random in the way the math assumed. It is self-organizing. It is at the edge of phase transition. It is alive.

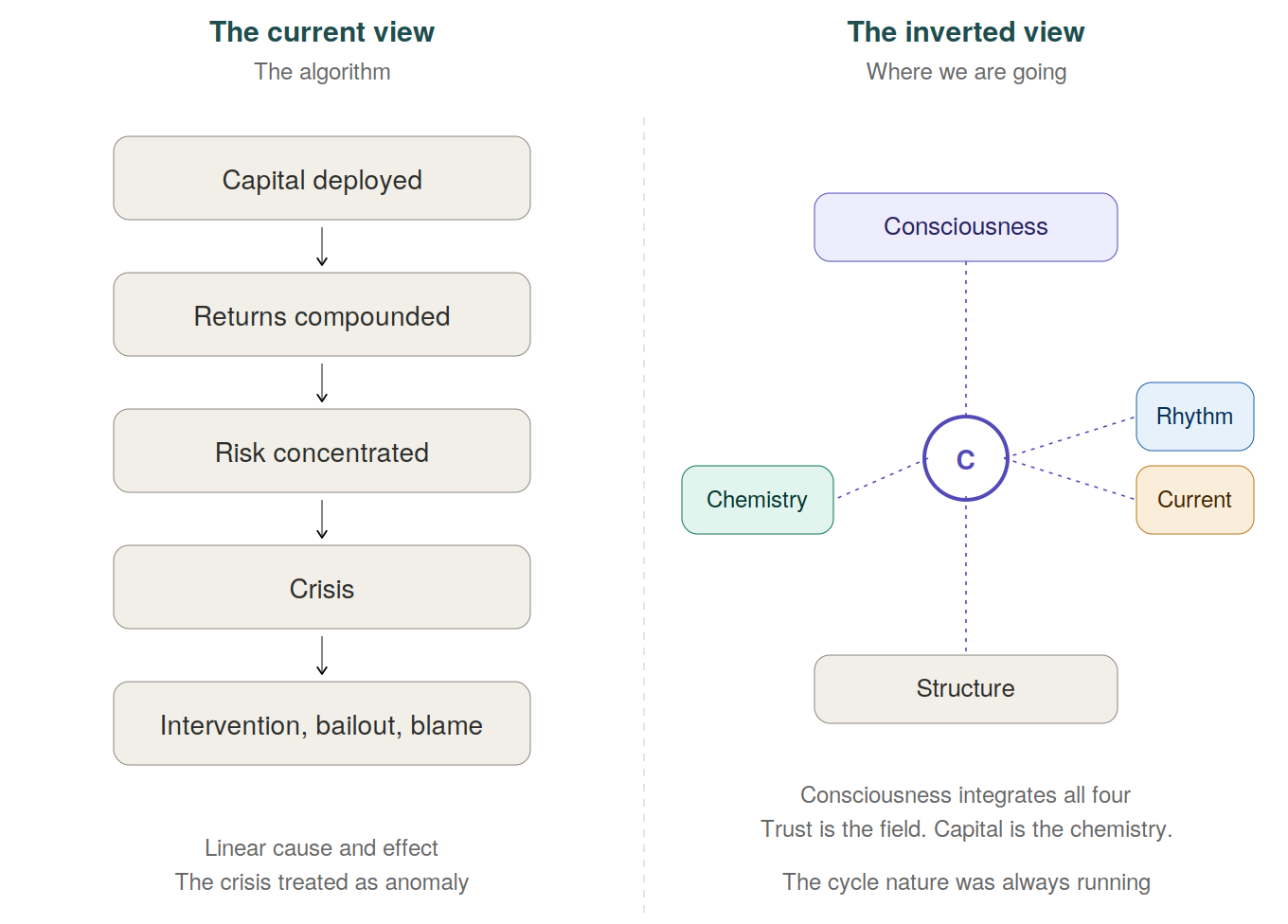

Here is the inversion. The current view treats finance as a structural and chemical mechanism that occasionally fails and needs the central bank to catch it. The inverted view treats the market as a four-layer event built from the relational and renewal logic every living system runs on. Every crash you have lived through is the market completing the renewal the algorithm forbade it to run at smaller scale. The 2008 crisis was decades of leverage, suppressed corrections, and concentrated risk arriving as one event. The Fed put created the conditions that made it inevitable. The recession is not a failure. The recession is the autumn. Autumn is how the system clears, frees trapped capital, returns the price of time to honesty, and prepares the next cycle. The industry that markets itself as the steward of the system has spent forty years preventing the autumn. The compounding cost of that prevention is what every body in the country is now distilling.

What’s Happening Overall

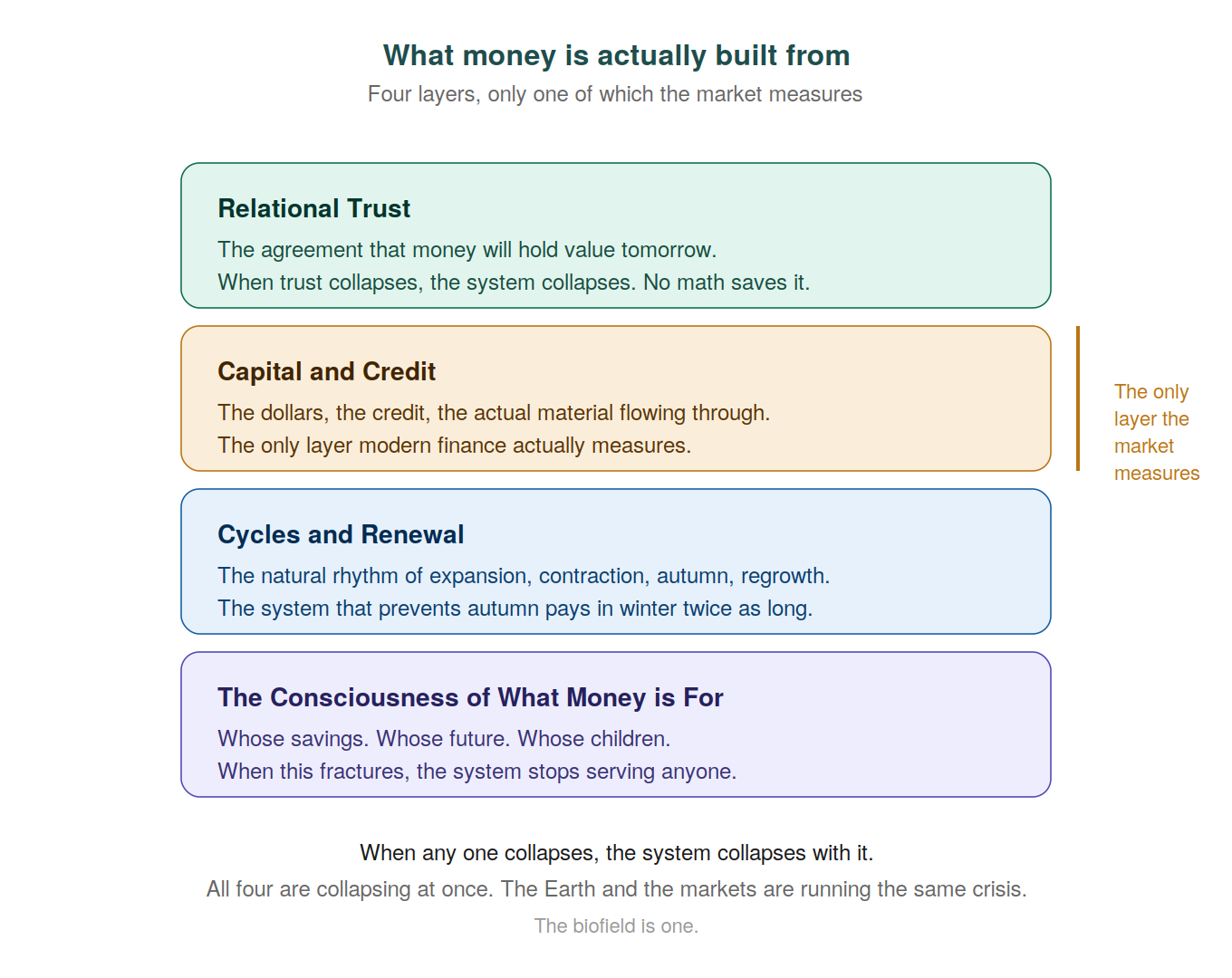

Money is built from four things, and the market only measures one.

Relational trust, the agreement between you and everyone else that the dollar in your hand will hold value tomorrow. When trust collapses, no math saves the system.

Capital and credit, the dollars and the debt and the actual material flowing through the system. This is the only layer the market actually measures.

Cycles and renewal, the natural rhythm of expansion, contraction, autumn, and regrowth. The system that prevents autumn pays twice as long in winter.

The consciousness of what money is for, the awareness of whose savings, whose future, whose children. When this fractures, the system stops serving anyone.

When any one of these collapses, the whole system collapses with it. And right now, all four are collapsing at once.

Look at all four layers collapsing at once. Trust in financial institutions is at historic lows across every demographic. Private credit has migrated more than $1.5 trillion dollars out of the regulated banks to a place where reporting is voluntary. Pensions are underfunded by trillions. The natural cycle has been blocked through five major interventions in twenty years, with each save building the foundation for the next, larger crisis. And the consciousness of what money is for has fragmented to the point where the largest pools of capital in the world cannot tell you whose retirement they are supposed to be funding. The Earth and the markets are running the same crisis at different scales. The mechanism is identical.

This is the through-line of the entire Inversion Series. The biofield is one. The polarization between Wall Street and Main Street, between capital and labor, between the financial economy and the real one, is the illusion the algorithm runs on. The unity is what the algorithm refuses to see. What you are reading in Finance, you are also reading in Climate (the Earth past her carrying capacity), in Insurance (the actuarial system retreating from the truth), and in Government (the polity unable to regulate the system that captured it). Same crisis. Different organ.

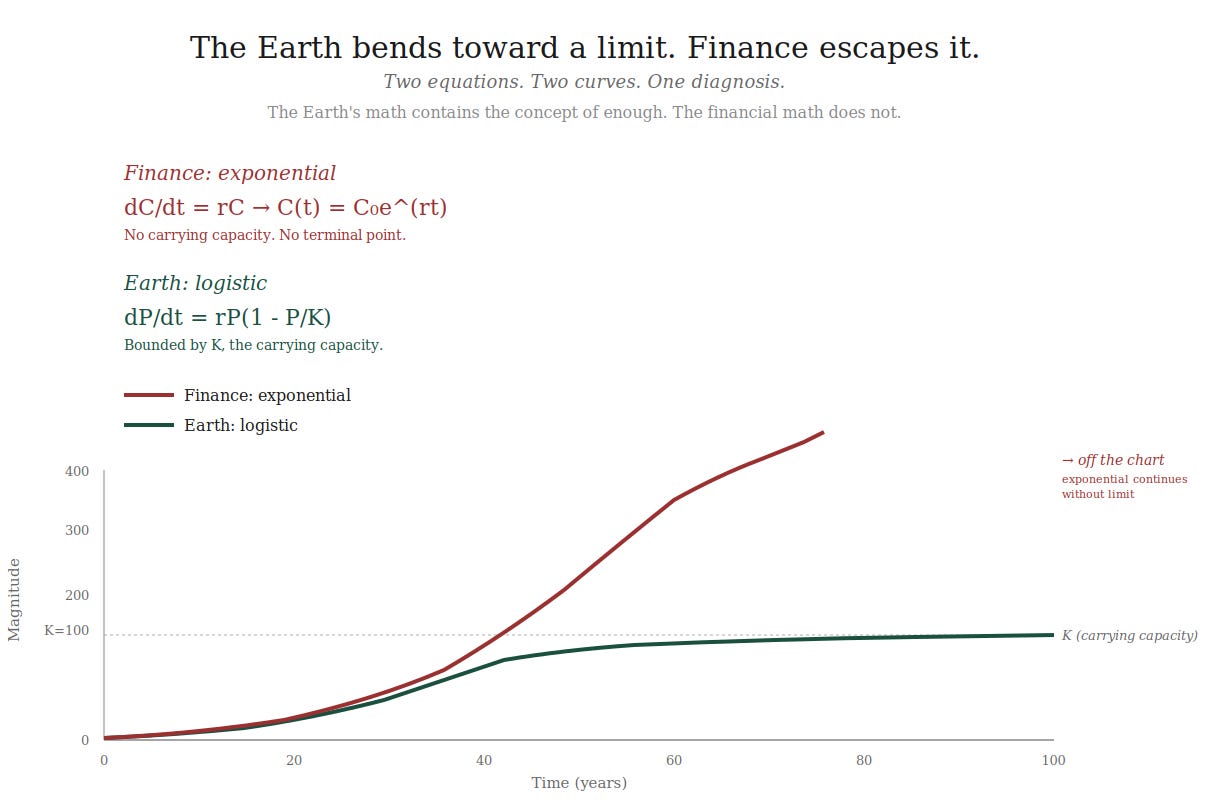

The math the industry uses came to us in stages. Harry Markowitz gave us modern portfolio theory in 1952. William Sharpe gave us the capital asset pricing model in 1964. Eugene Fama gave us the efficient market hypothesis in 1970. Fischer Black and Myron Scholes gave us the options pricing formula in 1973. Every one of these models assumes that returns follow a normal distribution, that markets clear at equilibrium, that actors are rational. All three assumptions were demonstrated false within a decade of being adopted. The math stayed in business school because the math was tractable, not because the math was right.

Then in 1971 the gold standard ended and the dollar became fiat. The Fed gained the ability to expand the money supply without any external constraint. The financial system stopped being tethered to anything outside itself. The system that had previously been forced to run through cycles by the underlying material reality became a system that could pretend to escape those cycles indefinitely. The compounding cost of fifty years of pretending is what every retiree, every working family, and every founder is now carrying.

My Experience & What I Witnessed

I have been working in finance from the operational side for fifteen years. I was a partner in a venture fund in San Francisco at the intersection of food, climate, and technology, where I watched capital flow toward whichever idea was telling the loudest story rather than whichever idea was doing the most honest work. Then I ran operations at a debt fund in Connecticut, which is where the full diagnosis arrived for me.

The companies in that fund could not manage their finances. They could not handle the operational load. The conditions kept shifting too quickly, regulatory, climatic, supply chain. The financial algorithm we had been running on no longer matched what the world was actually doing. Every company was over its head in debt, and every company was being asked to perform numbers that did not exist in the underlying reality of the business. I ended up inside the companies because the companies could not be inside themselves, and it burned my life down to do it.

In 2024, I went to NYC Climate Week as the CEO of Superstruct, which I had spun out of the debt fund to build a more sustainable structure. The week taught me something I had been circling for years. The financial system and the climate response system were built by the same hands using the same math. The institutions that funded the climate week were the same institutions whose business models depended on the system that had created the climate problem in the first place. There was no way to use those tools to solve the problem. The tools were the problem.

Here in Connecticut, I now pay roughly $15k dollars a year in property taxes on a small half-off-grid house in Simsbury. We do not have municipal water or sewage. The trash is my responsibility. The pond and its maintenance are my responsibility. The local energy grid is one of the most expensive in the country, and I run oil instead of natural gas because we are off the main lines. My children are homeschooled. We use the library. The library is the one part of the local financial system that still works as it was supposed to. Everything else costs more and delivers less than it used to, and the numbers I am asked to pay are getting bigger every year. This is the experience of nearly every American family at this point. The math has stopped working at the household level.

What the Experts are Saying

The lineages converge.

Frank Knight named the foundational error in 1921. There is risk, which can be priced because the probabilities are known, and there is uncertainty, which cannot be priced because the probabilities are not knowable. The whole modern financial industry runs on the assumption that uncertainty can be converted to risk through better models. It cannot. Hyman Minsky took this further in the 1970s with his Financial Instability Hypothesis, the observation that stability itself is destabilizing because it encourages the leverage and risk-taking that produces the next crisis. Minsky was largely ignored by the academic establishment until 2008, when his framework became the only one that explained what had happened.

Benoit Mandelbrot showed that markets are fractal, not Gaussian, and that the math the industry uses systematically underprices catastrophic risk. Andrew Lo’s Adaptive Markets Hypothesis treats markets as ecosystems rather than mechanical equilibria. John Fullerton’s regenerative capitalism work names the principles of finance that align with how living systems actually work. Mariana Mazzucato has been documenting for two decades that most of the major technological innovations of the past century were funded by the public and then captured by private capital.

“Stability is destabilizing.”— Hyman Minsky, 1986

And underneath all of it sits the lineage that the academy has been slowest to acknowledge. The indigenous economies that ran on gift, on reciprocity, on the seasons. The friendly societies and the mutual aid networks that managed risk through relationship. The commons that Elinor Ostrom won the Nobel Prize for documenting in 2009. The wisdom that capital has to be in relationship with what it is funding. None of this is new. All of it is what the modern financial algorithm has refused to learn.

Financial Events, Cover-Ups, and Chronic Conditions

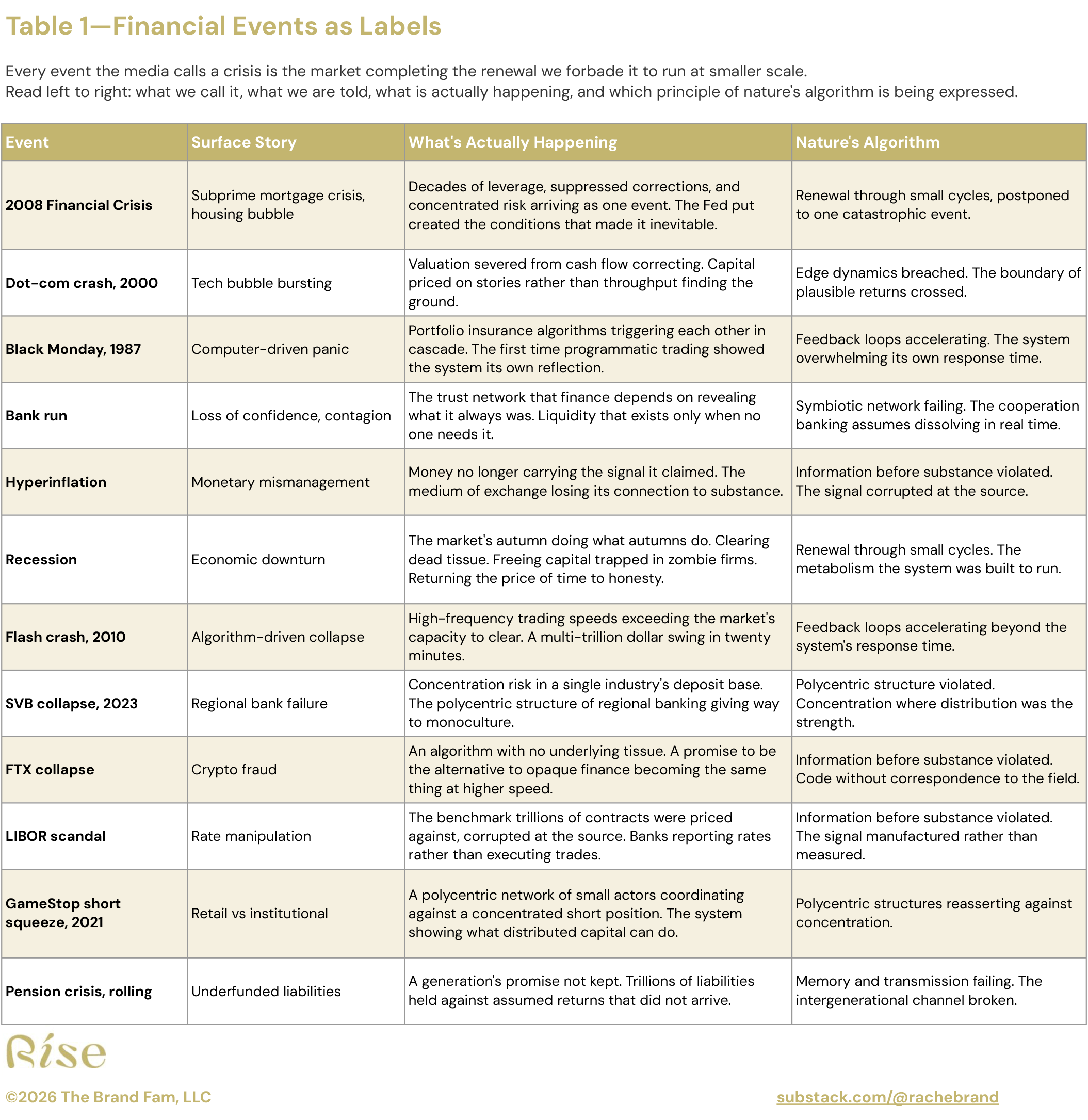

Every event the financial press calls a black swan is the market completing a renewal it was forbidden to run at smaller scale. The signal is the event. The event is the medicine we need to look at.

The 2008 crisis was the market’s wildfire, clearing what could not stay. Read this table left to right. Column one names the event we see. Column two is the surface story the system tells about it. Column three names what is actually happening underneath. Column four names the principle of nature’s algorithm the market is expressing. Every row is the system saying the same thing in a different language.

The benchmark the whole system runs on was manipulated for two decades by the same banks that set it.

Information before substance. The signal corrupted at the source.

For every signal the market sends, the modern system has built an intervention designed to silence it. The Fed put. Quantitative easing. The lender of last resort function expanded beyond recognition. The corporate bailout. The student loan freeze. The asset price floor.