Inversions: Insurance Sells False Safety & Security

Signal 055. You were taught that insurance is the responsible choice, the hedge against fate. The model assumed the tail would stay thin. We are in the tail now, the premiums fail the loss.

You have probably been taught that insurance is the responsible thing. You insure your home so that a fire does not bankrupt you. You insure your car because it is the responsible thing to do if you were to ever hit another car. You insure your life so that your family is taken care of when you go. You insure your health so that a diagnosis does not become a foreclosure. And what you believe is that the premium is the cost of safety and the claim is the system working.

The whole architecture of the modern adult life runs on insurance, and we have been taught not to question it. Actually, it’s irresponsible to even consider not having it.

Well, I have news for you before I write another word: We are tenants on this Earth and there is not a single dollar that can save you from what’s about to happen next.

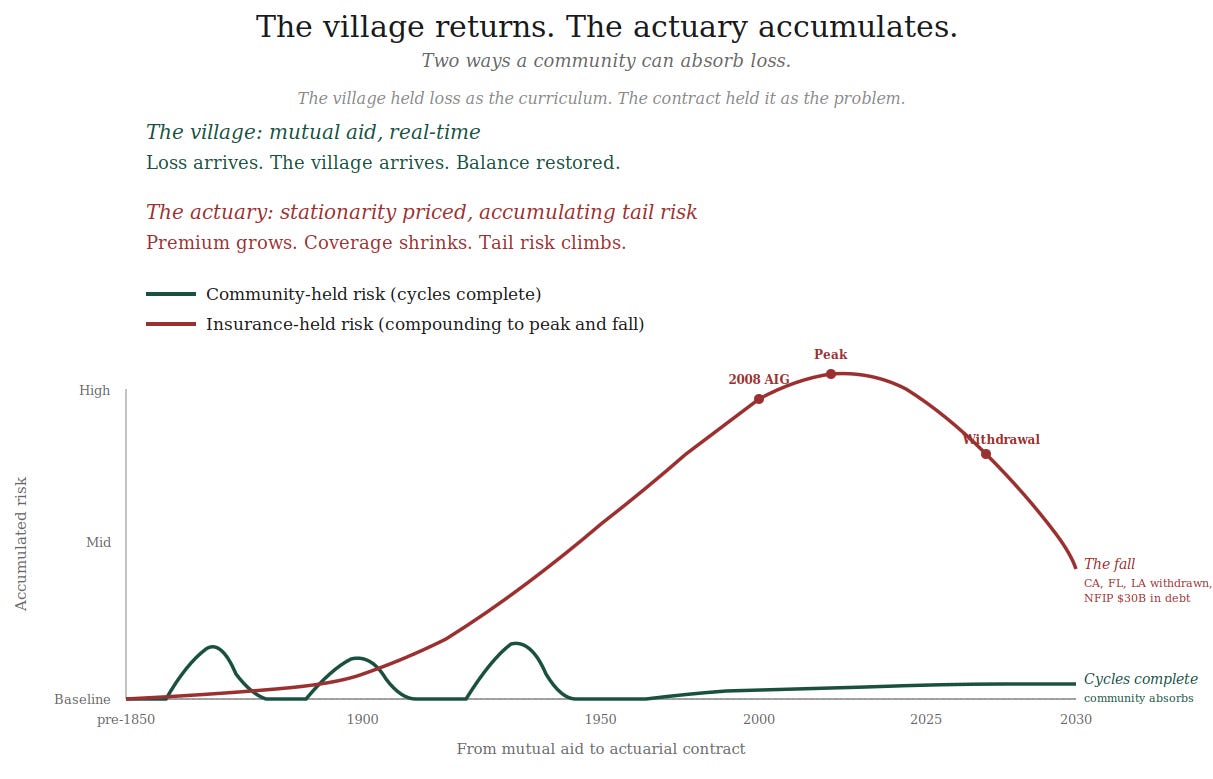

Some updates first on what’s actually happening in the US Insurance Market: State Farm, Allstate, and Farmers have stopped writing new home policies in California. Roughly thirty insurers in Florida have gone insolvent, withdrawn, or entered receivership in the last decade. The state insurer of last resort in Florida holds over a million policies it was never built to pay back and it won’t be able to. Long-term care insurance withdrew from a generation of policyholders because the math could not foresee a way to stay afloat. Cyber insurance tripled its premiums after NotPetya in 2017 because the algorithm could not price a risk category it had never seen and so now it is nearly impossible to insure some of these needs. Reinsurance is now retreating from climate exposure because the deepest layer of pricing has run out of ways to keep pretending the math works. The National Flood Insurance Program owes the US Treasury more than $30 billion, and they still keep covering expenses (which is crazy, keep reading below).

And this is only the current view.

It reads like they think they can fix the financial erosion they are living in. As if the government or the insurance market can somehow stabilize a system whose growing failures are technical problems to be solved with better modeling and more capital instead of looking at the long view. It is reading the symptom as the disease. It has been doing that since the mutual aid societies were absorbed into stock insurance companies in the late 1800s. The bodies are now telling us what that has cost, and it is the pressure and stress we are living in for no reason. And the Earth is about to tell us the rest.

What’s Happening Beneath the Surface

Now turn the reading… that’s right flip me upside down and reverse me and you might start to get it.

Insurance is just an illusion to keeping us from doing the work inside of ourselves. Believing we are the only safety that we could ever experience and it lives inside of ourselves. It is fear playing out in real time.

I think if you take anything away from this article, it's that we are missing the point of life. We are supposed to be on a journey that is laid out for us. When we intervene in the experience, we are just delaying what inevitably will come. We somehow believe that this 1 human life experience is all we get, and we need to enjoy it while we can and do whatever we can at all costs to have longevity and a full and robust material life, filled to the brim with entertainment, friendships, family, experiences…

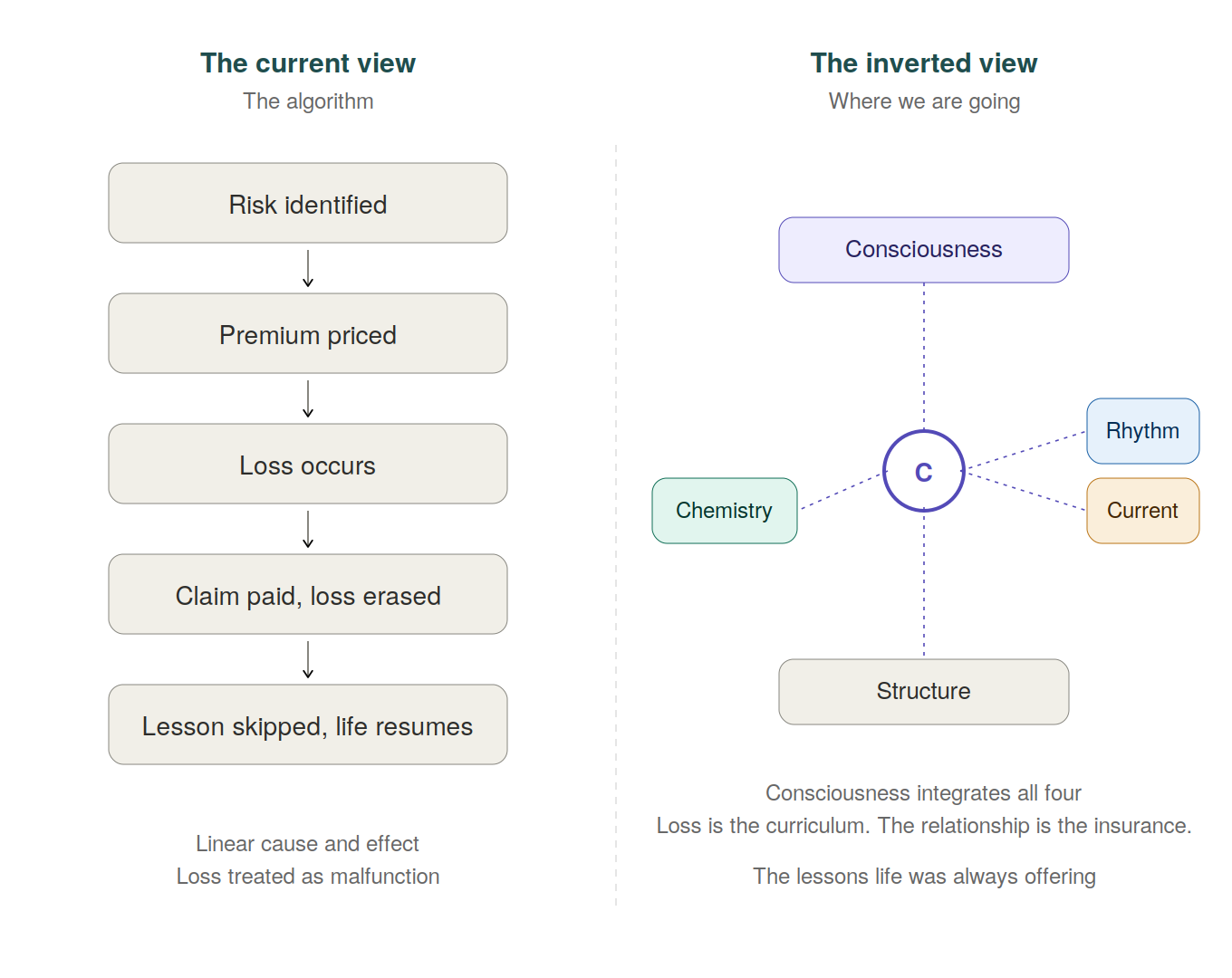

Insurance is the modern technology for opting out of the human curriculum. The fire is the lesson. The tree that falls on the car is the redirect. The diagnosis is the invitation. Death, birth, the hardship, the win, the four corners of the human experience, are not problems to be insured against. They are the flow of life, and the modern algorithm has been built to walk over every one of them and prolongue what comes next.

Here is the inversion: The current view treats insurance as the financial product that absorbs loss. The inverted view treats insurance as the spiritual error that absorbs the lesson. The body is not malfunctioning when the fire arrives. The body is being given the next chapter. The contract that pays the claim before the body has metabolized the loss is the contract that takes the upgrade and skips the integration.

And underneath the spiritual inversion sits a structural one. The math the industry has been running on assumes what climate scientists call stationarity, the assumption that the statistical properties of the past will hold in the future. The death of stationarity was declared in a 2008 Science paper (see references below) that the actuarial profession has been mostly trying to ignore. The premium you pay today was priced based on yesterday’s data.. isn’t that kind of funny? The almanac and the old news driving what we are doing today. The claim you file tomorrow will arrive under conditions that have already left the band the model was built to price. The system holds as long as today’s premiums exceed yesterday’s claims. The system fails when the conditions shift faster than the actuary can reprice. We are now in the moment when the math meets the field, and the field is winning.

Actually come to think of it, this is what we do with Laws too. We inform them off of old news, not what’s going to happen next. Facinating.

What’s Happening Overall

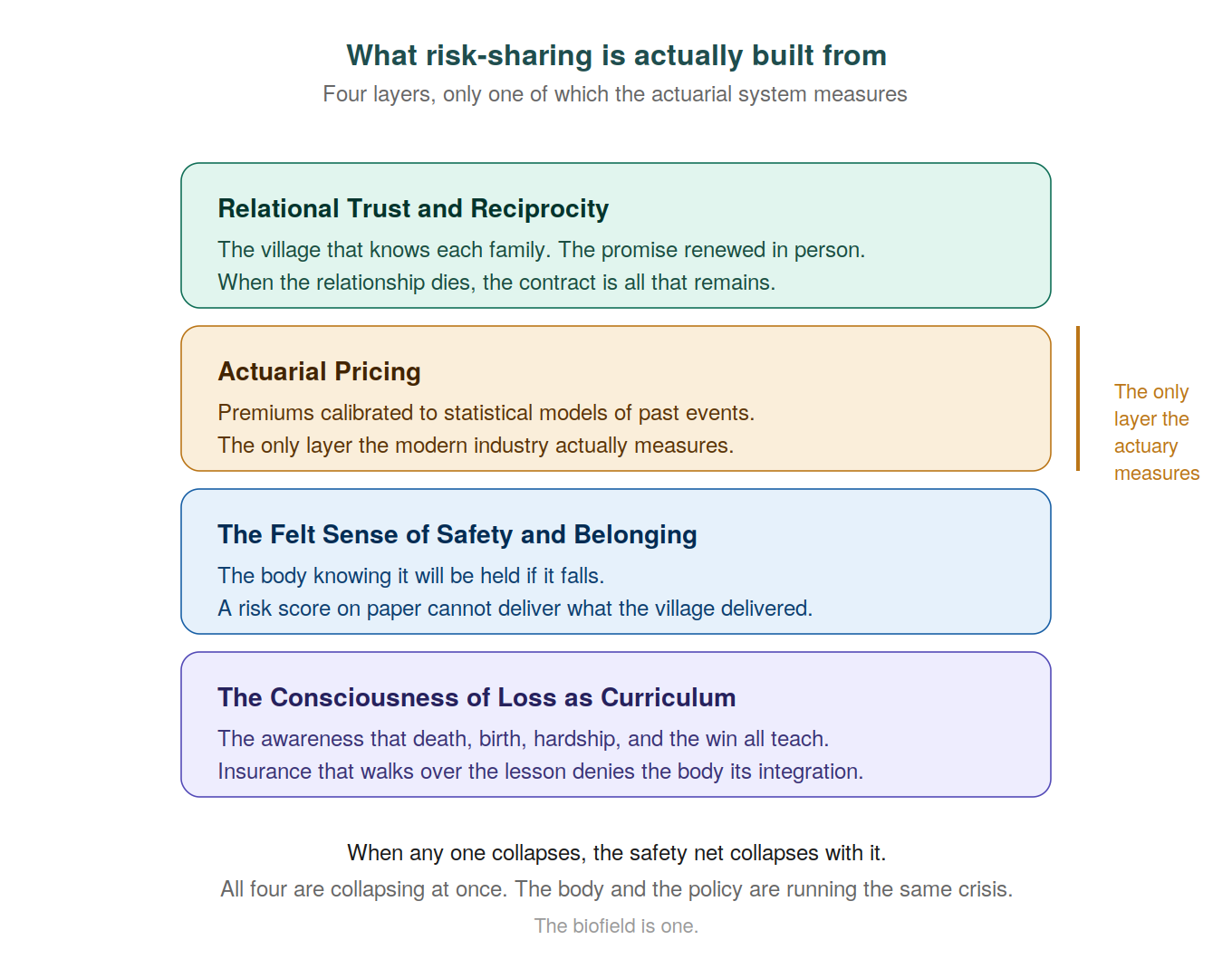

Real risk-sharing is built from four things, and the actuarial system only measures one.

Relational trust and reciprocity, the village that knows each family by name. The promise renewed in person at the church door, at the harvest, at the funeral. When the relationship dies, the contract is all that remains.

Actuarial pricing, the premiums calibrated to statistical models of past events. The only layer the modern industry actually measures.

The felt sense of safety and belonging, the body knowing it will be held if it falls. A risk score on paper cannot deliver what the village delivered.

The consciousness of loss as curriculum, the awareness that death, birth, hardship, and the win all teach. Insurance that walks over the lesson denies the body its integration.

When any one of these collapses, the safety net collapses with it. All four are collapsing at once.

This is the through-line of the entire Inversions Series. The biofield is one. The polarization between the contract and the relationship, between the policy and the village, between the individual buying coverage and the community holding each other up, is the illusion the algorithm runs on. The unity is what the algorithm refuses to see. What you are reading in Insurance, you are also reading in Climate (the actuarial system retreating from the Earth’s actual behavior), in Finance (the math of risk wrong from the beginning), and in Government (the institution that catches what the private market refuses to hold). Same crisis. Different organ.

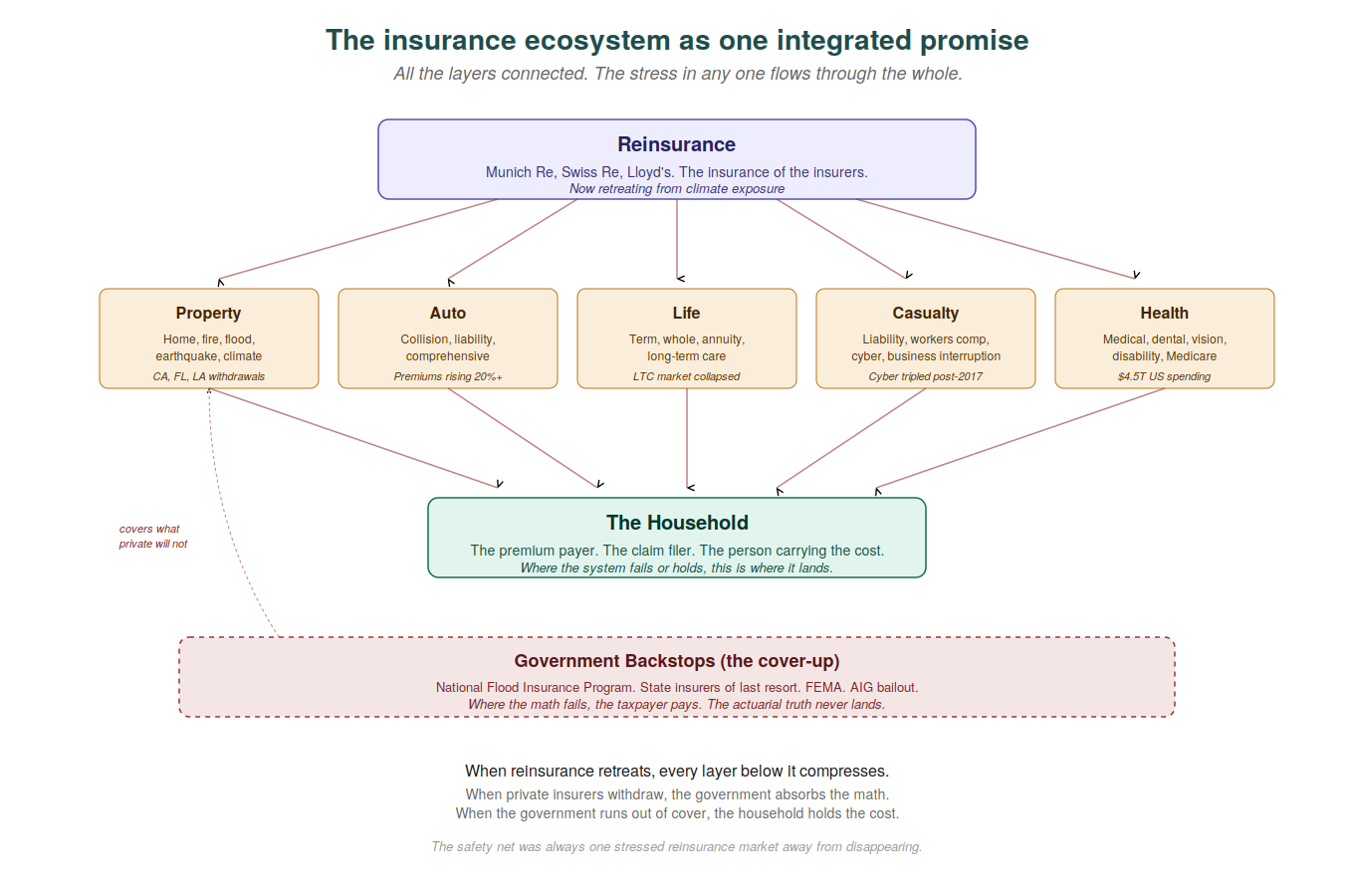

The Insurance Ecosystem as One Integrated Promise

To understand what is about to happen, you have to see how the insurance system works as one body, not as separate products. Property insurance, auto insurance, life insurance, casualty insurance, health insurance are not unrelated industries. They are linked at the top by reinsurance, the insurance of the insurers, and they are linked at the bottom by the household that pays into all of them. When stress arrives in any one layer, it flows through the whole structure.

Reinsurance, the insurance the insurance companies buy to protect themselves from catastrophic loss, sits at the top of the structure. Munich Re, Swiss Re, Lloyd’s of London, a small number of global institutions that absorb the worst-case scenarios so the primary insurers can keep writing policies. When reinsurance retreats from a category of risk, the primary insurers face capital constraints. They either raise premiums, withdraw from regions, or fail. Climate exposure has now hit the point where reinsurance is genuinely pulling back.

The five primary categories underneath the reinsurance layer all interact. Property losses from climate events feed into auto insurance through correlated damages. Life insurance and health insurance share actuarial assumptions about population mortality that are now diverging from reality. Casualty insurance, particularly cyber and business interruption, has seen premium tripling because the new categories of risk cannot be priced from historical data. Long-term care insurance is the canary, an entire product category that the industry quietly stopped offering because the math could not foresee modern longevity.

And the household, the family paying into all of these systems, sits at the bottom. When the layers above compress, the household pays more for less. When the household cannot pay, the government steps in. And this is where the cover-up runs deepest. The federal government has been absorbing the actuarial truth for decades through programs the average citizen does not know exist.

Lehman Was the Early Warning

In September 2008, Lehman Brothers collapsed. The headlines focused on the investment bank, the mortgage-backed securities, the housing market, the deregulation. The deeper story sat one layer up. American International Group, the largest insurance company in the world, had written credit default swaps insuring those mortgage securities at scale. When the underlying bonds began to fail, AIG could not cover the claims. The Federal Reserve and the Treasury extended a hundred and eighty-two billion dollars to keep AIG from going down, because if AIG had gone down, every major bank in the world would have lost its insurance on the assets it held, and the whole system would have stopped functioning the next day.

What the bailout revealed was the structural truth the industry had been hiding. The safety net the entire financial system was operating on did not exist. It was synthetic. It was priced. It was sold as if the math added up. The math did not add up. When the conditions the band had assumed left the model, the math could not deliver what the contracts had promised. The taxpayer covered the difference, and the system continued to operate as if nothing fundamental had been exposed.

Lehman and AIG together were the first major demonstration that the modern insurance architecture is a stability illusion built on a stationarity assumption that does not hold. Climate is the second demonstration and will be larger than the first because it is not a single contract category. Climate is the substrate underlying every insurance category.

The Government Cover-Up

In 2017 NPR’s Planet Money ran an investigation called Flood Money. The reporters profiled a man named Bill Pennington whose home in Houston had flooded every year for three years in a row. Each year, the National Flood Insurance Program paid out. Each year, he rebuilt in the same spot. The program could not drop him. The math was structural. One percent of insured homes have been responsible for more than twenty-five percent of all NFIP claims throughout the program’s history. The federal government has been paying to rebuild homes in places that everyone, including the actuaries, knows will flood again.

Selling flood insurance is a risky business. So risky that the private market refused to touch it decades ago. So the federal government stepped in. The NFIP now owes the US Treasury more than $30 billion. If it were a private company, it would be bankrupt. And instead of preventing risky behavior, the program may be encouraging it. The federal backstop is teaching homeowners and developers that the actuarial signal does not matter, because the cost will be socialized.

This is the cover-up. The government is absorbing the math that the private market has been showing for decades. Every time a community rebuilds in a flood zone, every time FEMA writes a check, every time a state insurer of last resort adds a million new policies, the underlying truth is being suppressed. The truth the actuarial system has been telling is this: large portions of the modern built environment are uninsurable at any honest price. The government has been holding the bag, and the bag is getting too heavy to hold.

When the federal government runs out of capacity to absorb the math, the household bears the cost. We are approaching that moment now. And the political response to it will be the next chapter of the Government Signal in this series.

My Experience & What I Witnessed

I have a few stories I want to share with you you, because the diagnosis I am writing about here lives in the body and the data is what it becomes on the other side. We actually KNOW this inside of us, but we ignore the nagging and surpress it through more material noise.

The house that burned to open the path

In many cultures, a house burning down would be a celebration as I wrote about in the original inversion. I dated a man whose home burned down in 2012. He needed to work through some major family stuff at the time with his parents and his upbringing, and he had brand new twins and two young kids. The twins, 1 of them had a compromised situation from birth that needed to be dealt with. And the burning was to slow him down. But instead, he put his head down, muscled through, and turned the situation into an investment opportunity through insurance. Bravo B, you still have to do the work on your mind at some point in some lifetime.

The property had been worth roughly $800,000, maybe $1.2m with all their stuff, I can’t remember. The insurance company paid out, and he used the money to build a new house worth $3.5 million. He took the upgrade and he spent 18-months focused on the rebuild. He never sat with the loss. He never asked what the fire had come to teach him. The new house was larger, brighter, more impressive than the old one, and he was the same man inside it. The insurance had given him more financial value and created a deficit in the inner work the experience was designed to do. The point of the effort was missed. He walked over the lesson and kept walking, and his daughter was 17 and living on a feeding tube after a brain tumor was removed last April. He divorced his wife, running away from his problems, instead of running towards them, suppressing them with wellness tricks like Breathwork. The daughter was standing in the middle, trying to do her soul’s work to bring him back to his center. And he can’t hear her… even still.

Remember, a burning will always mean that you are a phoenix ready to rise if you only pay attention to it.

Energetic Suppression through Life Insurance

I have always been uncomfortable with life insurance, even though I had various policies for most of my life. Actually, it was an endless thing in my family because my father couldn’t get one after he was sick, but they took a policy out in my name with both my parents on it when I was 3. And because they got divorced, I couldn’t access the policy until we tracked down someone who could support me in converting off of both of my parents’ death benefits into a whole life benefit, and by the time I received the money for the policy, I used it to go through my own divorce in 2024—kind of crazy to imagine how long it took. It was a direct exchange. A very low 1% growth on that policy since 1984… almost exactly what my parents put into it.

My family felt getting an insurance policy was critical and that it was irresponsible not to have one so I got a term life policy and paid $325 a month for 20 years. That money instantly evaporated. The premise of the Life Insurance product is that you pay a small amount over the years so that when you die, your family receives an amount like a security policy.

In the actual transaction of a Life Insurance payout, the death is converted from a negative loss to a positive balance sheet: the energetic register is a loss, but the accounting register is a gain. The two registers do not match; in fact, they are reversed in logic. You should have the energetic release that the soul is doing the work it needs to do, and in some ways, it is an energetic gain or a graduation beyond this 3D dimension. The accounting register should be the loss that you feel, and instead of grief, you are working through the next stage of your own development.

The reality is that this mismatch sits in the body, and we are so uncomfortable in grief because we are in conflict between the two. We are basically offering a penance to go through the loss and have a backup plan for the family we are leaving behind. There is something there that has always made me uncomfortable. The product is built on the assumption that the family will integrate the grief more effectively if they have the check. I know now that the money sits there like an open wound until you put in the time you need to grieve.

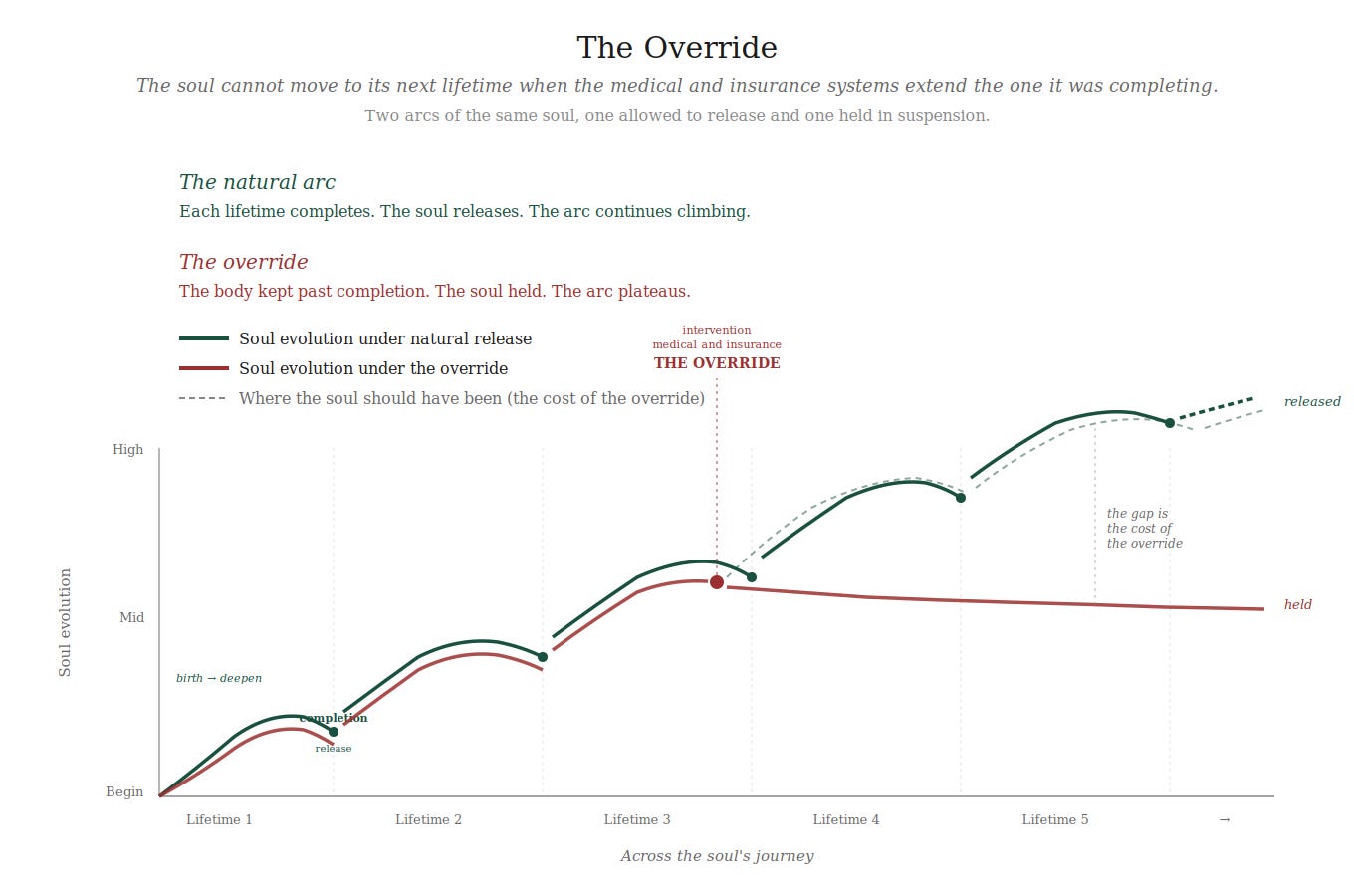

The intervention is what elongates the pain

I have to write it carefully because I am still inside it. My father was diagnosed with AML when I was fourteen. He is alive today, thirty-one years past the bone marrow transplant, one of the longest living survivors. He is in hospice now. The medical system kept him alive past what I believe was his natural timeline. The interventions extended the life. The insurance system covered the interventions.

I am grateful for those years so it is bittersweet to even talk about this. He met my children. We did real work together in the last few years, work that would not have happened if the system had let his original timeline run to completion. I am grateful, and I also believe the system screwed up the timeline. When we use intervention to override what the body is doing, we are screwing up the concept of what was supposed to happen. The thirty-one years are a gift I would not trade. The override is also real.

The risk comes from the insurance and playing with nature’s inherent gifts

In Guatemala I learned that birth had become surgery. In the private hospitals of the cities the cesarean rate runs near 90%, in the public hospitals near 50%, and in the villages a 15%, where many mothers cannot reach a surgical hospital at all. The World Health Organization names 10% to 15% as the rate that meets medical need. Above that line the cut tracks money and access.

For a long time, I could not place what I was seeing. Even without the intervention of cutting open, these women were all taking drugs, and their first moments with their precious life were tainted forever. The mother takes an epidural in the spine, the contraction loses its feeling, the labor slows, and Pitocin goes in to push it forward. Pitocin is the body’s own oxytocin made synthetic, and it moves the muscle of the uterus while staying out of the brain, so the contraction arrives without the current that should carry it. The body is numbed first and driven second. The birth is performed.

Which, for the life of me, I couldn’t understand why anyone would want to do.

But to then get cut open? There had to be some kind of reason. In Guatemala, many of the affluent women wanted to plan their deliveries and the doctors wanted to show up there at their best and be rested. It was very inconvenient in the middle of the night. Additionally, it was always nice to have family coverage for your other children and a driver on standby. And INSURANCE preferred it. It offered a much easier way to plan and to insure the quality of birth went off without a hitch.

So they played their hand outside of nature and created the master of their own destiny. How crazy to imagine. In the US, the statistics are rising too… mostly because it is better for insurance companies not to have emergency scenarios and put the mother at risk.

My friends who have had a cesarian have a 6-week recovery time. I had a 2-hour recovery time, and I happily walked around and hugged my babies. We went to the museum 36 hours after giving birth with Iza.

These stories sit in the same diagnostic. Insurance, when it does its job most efficiently, is not delivering safety. It is delivering an exemption from the experience that the body came here to have. The fire was supposed to teach him. The death was supposed to be metabolized in real time. The illness was supposed to complete its arc. The birth is a natural order of connection and receipt. We have built a system whose entire purpose is to interrupt these arcs, and we have called the interruption progress.

What the Experts are Saying

The lineages converge.

Frank Knight named the foundational error in 1921. There is risk, which can be priced because the probabilities are known. There is uncertainty that cannot be priced because the probabilities are not known. The whole modern insurance industry runs on the assumption that uncertainty can be converted to risk through better models. It cannot. Hyman Minsky’s Financial Instability Hypothesis describes the second-order consequence. Stability itself is destabilizing because the appearance of safety creates the leverage and risk-taking that lead to the next crisis.

Peter Bernstein’s Against the Gods documented the four-hundred-year history of how humans came to believe risk could be tamed. The book ends with the warning that we had built a civilization on the assumption that uncertainty could be managed mathematically, and that the assumption had never been tested at the scale it would eventually be tested. The test is now.

Jonathan Levy’s Freaks of Fortune traced the cultural shift through which Americans came to understand themselves as risk-bearing economic actors rather than as members of communities that collectively absorbed loss. The shift happened in the late 1800s. The friendly societies, the burial associations, the mutual aid networks, the Quaker meeting houses, the Catholic confraternities, the African American burial societies, the union locals were absorbed into stock insurance companies that treated the policyholder as a customer rather than as a member. The premium became a transaction. The relationship died.

Elinor Ostrom won the Nobel Prize in 2009 for demonstrating that commons work all over the world. They have always existed. They still exist. The polycentric governance of shared resources is the deepest model of how human beings actually manage risk in community, and it has operated in parallel with the modern insurance industry for the entire time the industry has been claiming there was no alternative.

“Risk is what you can put a number on. Uncertainty is what you cannot.”

— Frank Knight, Risk, Uncertainty and Profit (1921)

And underneath all of it sits the older lineage. The Quaker meeting decided collectively how to support a family in hardship. The Amish system that still operates today, with no insurance at all because the community is the insurance. The Jewish chevra kadisha. The Catholic confraternities. The harvest festivals in every traditional culture brought the village together to celebrate abundance and quietly distribute the surplus to the families who needed it most. These were not folk customs. These were the operating systems of human risk-sharing for thousands of years before contracts replaced relationships.

The Harvest Festival as Risk-Sharing Technology

Every traditional culture has a harvest festival, and the festival's structure is identical across continents. The village gathers. The harvest is brought in. The surplus is shared. The families who had a hard year are fed first. The wealthy families contribute the most. The poor families contribute what they can. The next year, the roles may switch. The whole system functions as continuous mutual insurance through ritual time.

The harvest festival was never a celebration of abundance. The harvest festival was a social technology for distributing risk across a population that recognized itself as one body. The acceptance that life contains death, birth, hardship, and win was the underlying premise. None of these were problems. All of them were the curriculum. The community gathered to celebrate that we were all in it together, that nobody escaped the four corners, that the way to live with loss was to make it visible and shared rather than private and absorbed by contract.

The modern equivalent does not exist. We have Thanksgiving as a vestigial form. We have birthdays as private rituals. We have funerals as small private affairs that close in a few days instead of the month-long experiences in the past. The civic technology for celebrating loss as part of life, and distributing the cost of being human across the community that shares the life, has been almost entirely dissolved. The insurance contract is what replaced it. The contract pays. The community no longer arrives.

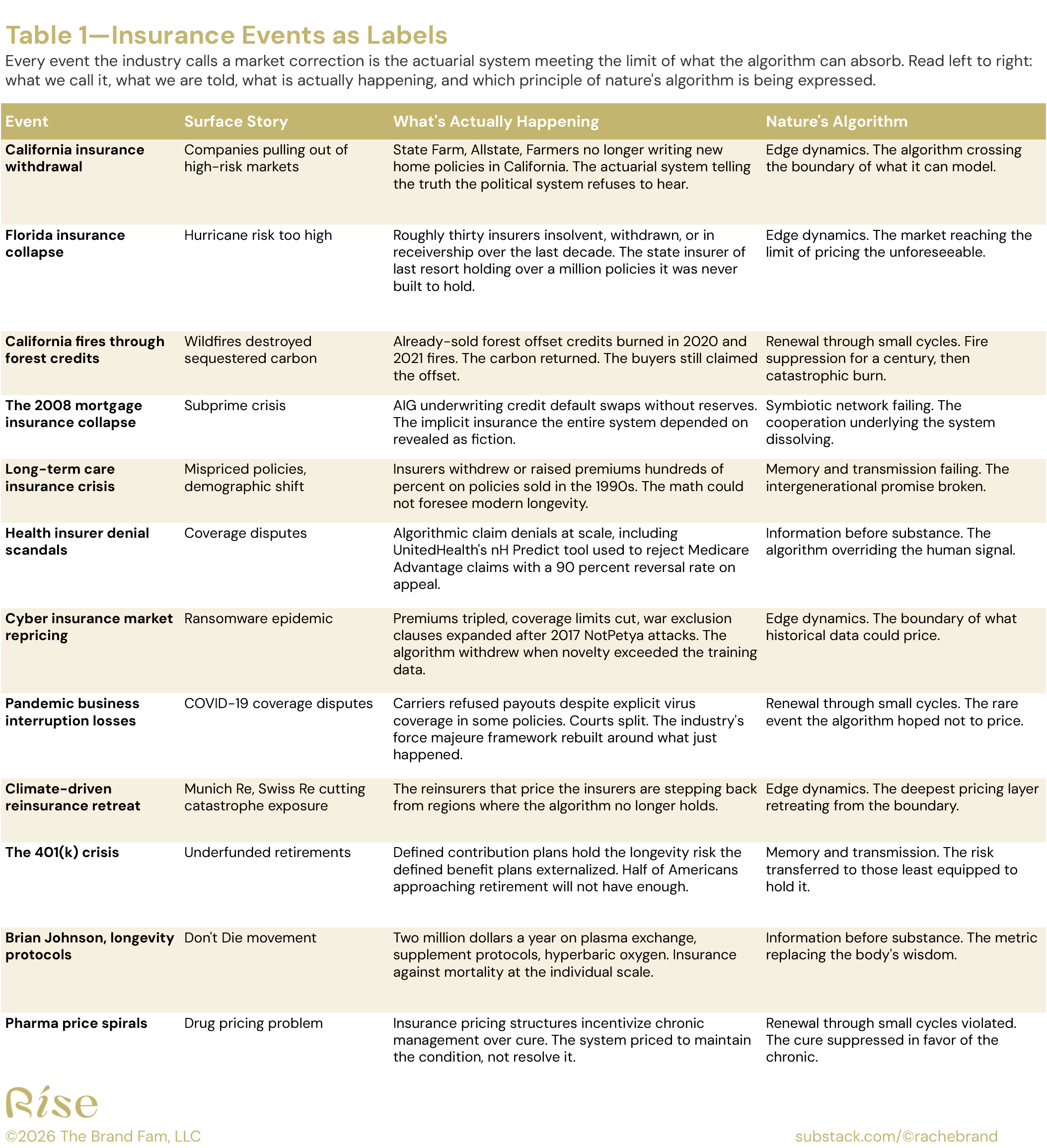

Insurance Events, Cover-Ups, and Chronic Conditions

It’s like we are falsifying each event without realizing it.

Every event the insurance industry calls a black swan is the system completing a renewal that was forbidden to run on a smaller scale. The signal is the event and this event is the medicine we need to assume is right.

Read this table left to right. Column one names the event we see. Column two is the surface story the system tells about it. Column three names what is actually happening underneath. Column four names the principle of nature’s algorithm the body is expressing. Every row is the system saying the same thing in a different language.

For every signal the body sends about loss as curriculum, the modern system has built an intervention designed to silence it. The insurance check that arrives before the grief lands. The settlement that closes the case before the lesson is metabolized. The lump sum that builds the bigger house. The death benefit pays the family before they have felt the loss.